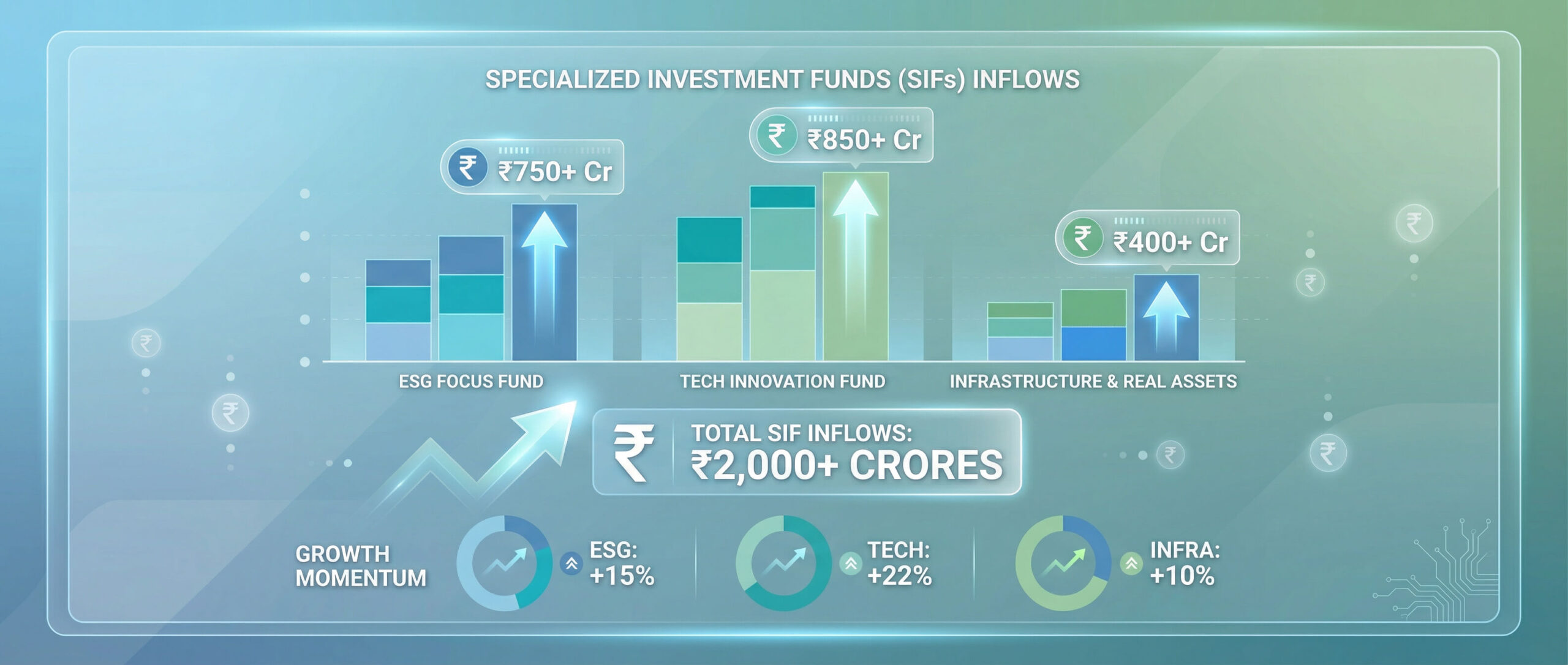

The first four schemes under the Specialised Investment Funds (SIFs) as allowed by SEBI were launched by different AMCs. These SIFs make use of derivatives in a way which cannot not done by mutual fund schemes. Hence the minimum investment amount in such schemes is Rs ten lakhs. The first schemes under these category were launched by Asset Management Companies during October 2025 and garnered more than Rs 2,000 crs.

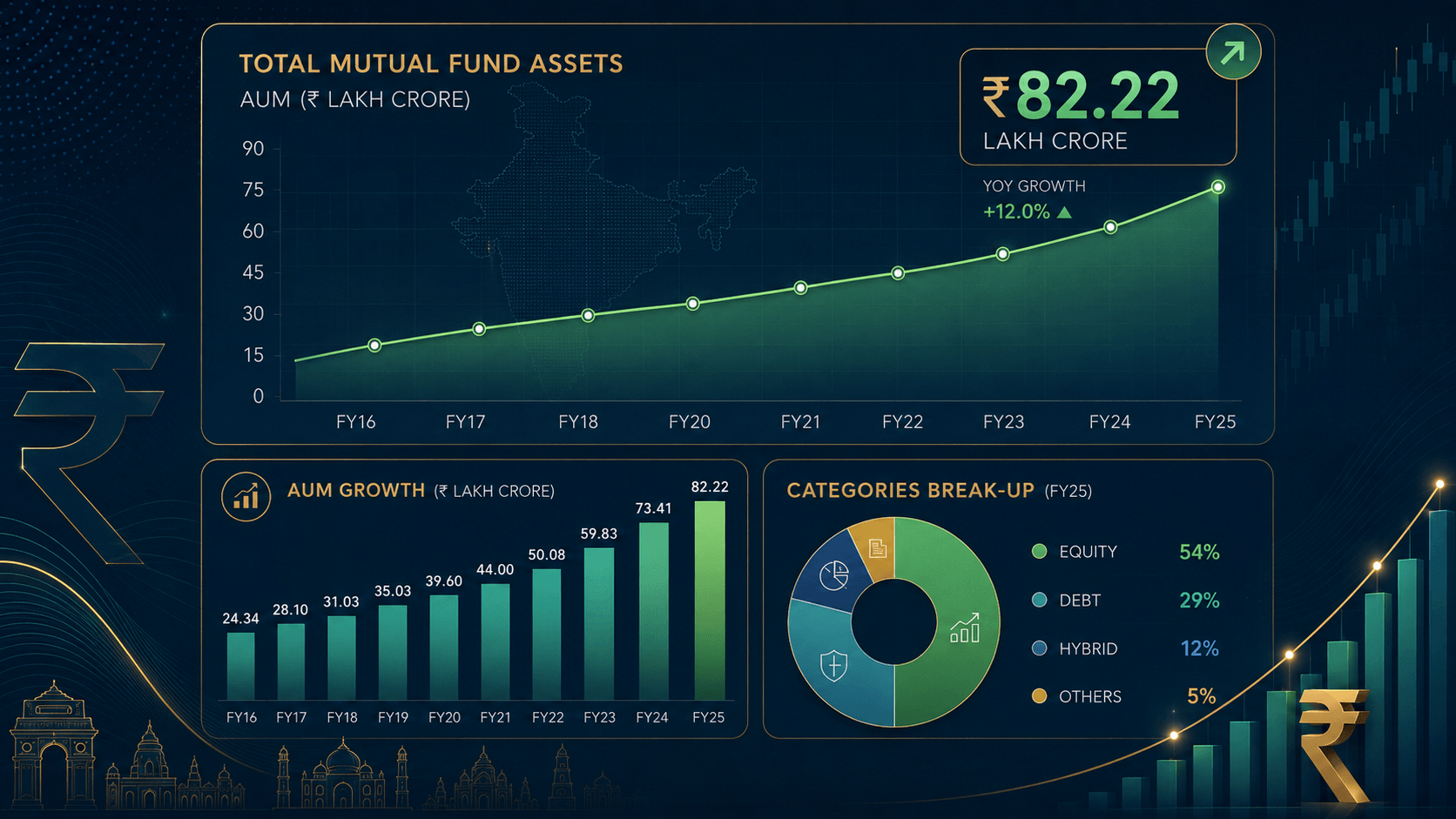

Indian mutual fund industry ended October 2025 with assets of Rs 79.9 lakh crores compared to Rs 75.61 lakh crores in September 2025. The AUM of the industry has doubled over the last three years. The Industry witnessed net inflows of Rs 2.15 (0.43) lakh crores, with debt schemes garnering 1,59,000 crs and equity and hybrid schemes showing net positive inflows of Rs 24,690 crs and Rs 14,156 crs respectively. Equity schemes saw an increase in assets to Rs 35.2 (33.68) lakh crores. This was mainly due to the positive performance of the markets as well as net inflows. Nifty 500 moved up by 4.37% and Nifty 50 increased by 4.62% with mid and small caps also up. One year returns for all indices are slightly positive. Three and five year numbers continue to show healthy returns inspite of the near term blip.

Mutual Fund Industry Overview

🔹 Monthly flow and AUM trends:

Equity Mutual Funds :

– Net flows in equity schemes fell to Rs 24,690 crs from Rs 30,422 crs last month. This has been the fourth consecutive month of decline in inflows. Though there have been no negative inflows for almost five years. Flows have declined inspite of six new NFOs collecting almost Rs 4,000 crs.

– AUM of flexi cap funds is now almost the same as all thematic/sectoral funds. This is a good thing as flexi cap funds should be less volatile then thematic funds. Flexi cap funds had the highest inflows followed by mid and small cap funds. SIP inflows were at Rs 29,529 (29,361) crs and were marginally higher than last month continuing the uptrend of the last few months.

– Net inflows in various categories were as under and have declined compared to last month. ELSS and Dividend Yield funds saw net outflows:

– Sectoral/Thematic Funds: ₹ 1,336 (1,221) crores

– Flexi-Cap Funds: ₹ 8,928 (7,029) crores

– Small-Cap Funds: ₹ 3,476 (4,363) crores

– Mid-Cap Funds: ₹ 3,807 (5,085) crores

📌 #EquityFunds #MutualFunds #WealthCreation #LongTermInvestment #EquityMarket #ELSSschemes #Equityschemes

Debt Funds: Inflows due to the beginning of the financial year/quarter

📉 Key Trends in Debt Funds:

– Total debt fund AUM was ₹ 19.51 (17.80) lakh crore, a 9.6% increase compared to last month and up by about 17.3% compared to last year.

This category saw a net inflow of Rs 1.6 lakh crs compared to an outflow of 1.01 lakh crs last month. Most debt fund categories saw net inflows highest inflows after liquid funds.

#DebtFunds #InterestRates #BondMarket #FixedIncome #FinancialPlanning

Hybrid & Passive Funds:

– Hybrid funds’ assets increased to Rs 10.70 (10.33) lakh crs thus staying above the ten lakhs crore mark. A 22.6% increase over the last 12 months. Net inflows into hybrid funds stood at Rs 14, 156 (9,397) crores, led by Arbitrage and Multi Asset Allocation funds, which saw inflows of ₹ 6,930 and Rs 5354 (4,982) crores in October. Arbitrage funds saw inflows. Given the volatility of the equity markets, multi asset funds should provide stable returns going forward till earning catch up with valuations. Equity savings and balanced hybrid funds saw a decrease in inflows.

📌 #HybridFunds #Diversification #RiskManagement #BalancedInvestment

Passive mutual funds:

AUM of passive funds rose 5.2% to 13.67 (12.99) lakh crores on the back of a surge in gold prices and rising inflows into these funds. AUM of God ETFs crossed Rs 1 lakh crs and reached Rs 1.02 lakh crs. Gold ETFs inflows were Rs 7,743 (8,363) crs. Gold and silver have seen a big jump this year.

🧐 Way forward

Most indices have given a negative return over the last one year. The markets have been volatile too. Indian macros continue to be strong. The recent cut in GST rates as well as the cuts in income tax at the beginning of the year should aid consumption. The headwinds continue to be US tariffs as well as other policy related matters with other countries. Investors are suggested to continue investing via SIPs and STPs. Lumpsum investments in equities should be avoided. Arbitrage and short term debt funds can be used to park funds and moved to large cap or hybrid schemes over the next 8-12 months. The asset allocation to different asset classes should continue to be maintained.

About EquiZen

EquiZen, a registered mutual fund and PMS distributor, offering personalised financial solutions with a focus on safety and transparency. We aim to assist you to achieve financial freedom, the freedom to do what you want and achieve your dreams. We do not push financial products but believe in utilising them judiciously to meet your needs. Learn more at www.equizen.in or contact us via +91 9820605203 or sanjay@equizen.in.