In this post, we analyse the assets and the flows in India’s mutual funds industry in the month of July 2024.

Total Assets Under Management (AUM)

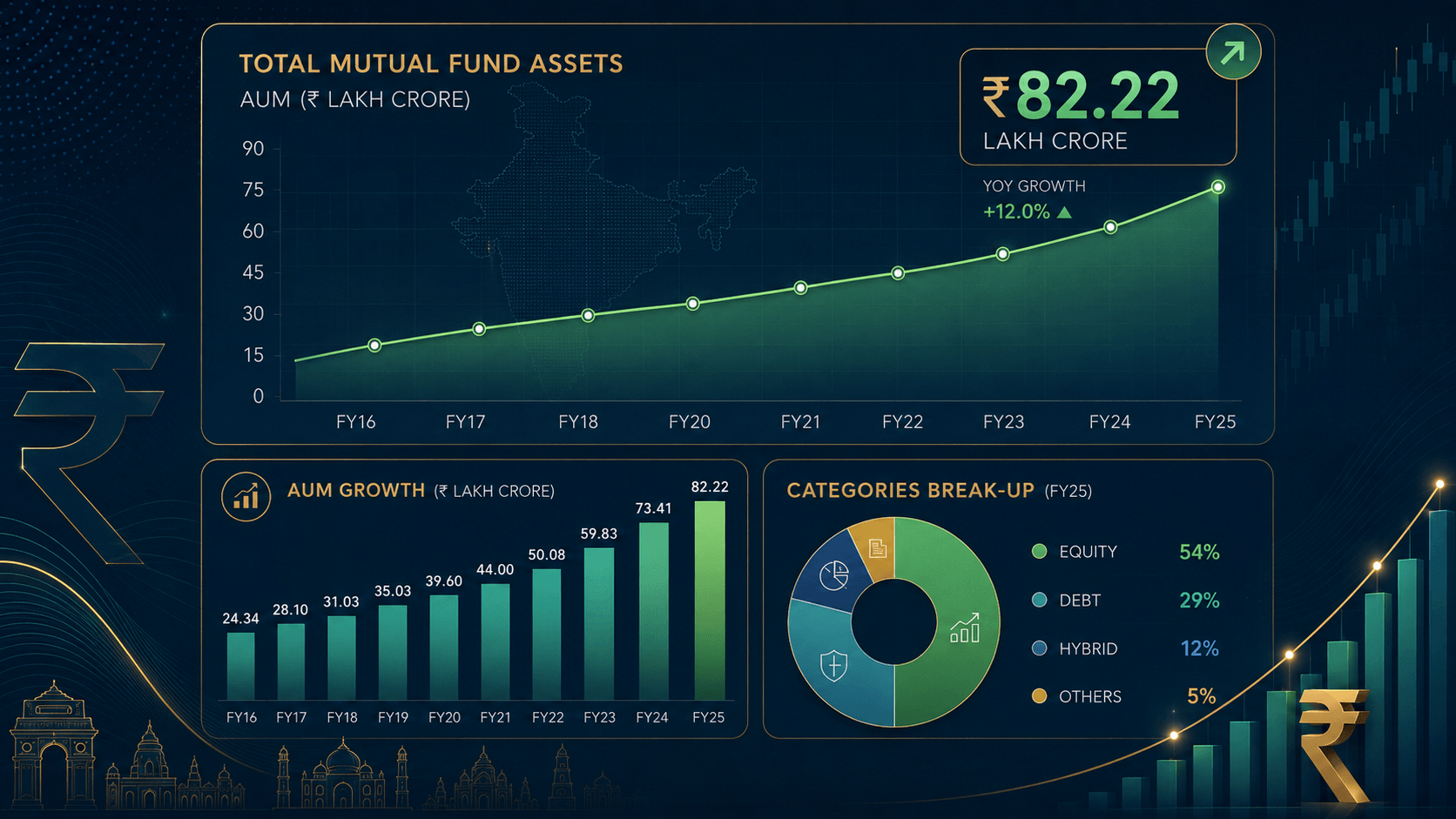

Total AUM of all schemes was close to Rs 65 lakh crores. They would have crossed this number by now and we can be sure that the August month end numbers will cross the 65 lakh crs mark. This is a 6.23% growth over the previous month. Total AUM was Rs 46.37 lakh crs in July 2023. The jump of 40% is substantial. AUM of equity oriented schemes jumped by 61% over a year. These are the money making schemes for Asset Management Companies and the bottom-lines of these companies will see a huge increase in the current financial year. AUM of Hybrid schemes has also shown a very good growth of 53.45%. Most of this growth seems to have been driven by Arbitrage schemes. Their AUM increased from Rs 90,745 crs to 189,349 crs. Are all the profit booking flows invested here? Are people switching out from Equity to Arbitrage schemes or are they redeeming from equity schemes and investing in Arbitrage schemes? We need more data to determine the answers to these questions.

Are investors trying to time the markets? Will they get back in once the markets reach a reasonable level. How will they determine what level is reasonable? Are their advisors good enough to give them this advice? Should the advisors not be focussing more on ‘time in the market’ rather than ‘timing the market’?

Equity and Hybrid schemes

Gross inflows in equity and hybrid schemes in the month of July were mostly unchanged compared to June 2024. Gross inflows have doubled over July 2023. Gross inflows in these schemes increased to Rs 127,000 crs from Rs 64,000 crs. Net inflows in July were ten percent more than in June. They were at Rs 54,500 crs. Net inflows in July were a whopping 272% more than last year. Last year net inflows were only Rs 20,000 crs. This is a very large increase and probably one of the reasons why markets are either stable or creeping up. Net inflows in mid cap and small cap funds are lower than last year. Old investors are booking profits. But new investors seem to be attracted by the good returns over the last few years.

Most of the gross inflows still come to sector schemes. There were two NFOs which garnered 9,790 crs of assets. Gross inflows in sector funds last year was Rs 6,192 crs which have increased to Rs 27,468 crs in July 2024. Net inflows have grown from Rs 1,429 crs to Rs 18,386 crs. That’s a massive jump. The second biggest category was multi cap schemes followed by Flexi cap schemes. Mid caps and small cap funds raked in Rs 7,000 crs each approximately.

Are investors investing in sector funds as also mid and small cap schemes based on their strategic asset allocations? Or are they just investing in these funds from a tactical perspective? Does it make sense to invest in the markets at these levels. Most market participants believe that there is value only in large caps. However, large cap schemes are seeing very less net inflows in July as well as in June this year and the story must be the same for the rest of the months. Last year, in fact, they saw net outflows. Are investors expecting the market to keep giving double digit returns over the next few years. Will they be disappointed if they see single digit returns and if that happens, will they stop investing or even worse redeem to chase that asset class which has given higher returns. And which asset class will that be that will be the next multi-bagger? Are AMCs doing the right thing by launching so many new schemes and garnering AUM in sector schemes? Are they being customer centric or only AUM and hence bottom line focussed? Do they consider the present value of a customer who invests with them for a life time vis a vis a customer who invests in the hope of quick and high returns and leaves after getting disappointed. Are advisors advising their clients that they may have to stay invested for much longer periods from now onwards compared to what they have seen in the past. Long term returns are around 20%. Markets may have to see a correction in order to revert to the mean and nobody knows whey that will happen, how deep will it be and for how long will it last.

There are 174 sector schemes. They have 2.47 cr folios out of the total 19.84 cr folios. They are followed by small cap schemes with 2.08 cr folios. ELSS, Flexi and mid cap funds have 1.5-1.6 cr folios. None of the hybrid schemes have more than 1 cr folios. The largest being Aggressive Hybrid funds with 55.1 lakh folios. Not surprisingly, Arbitrage funds have only 5.32 lakh folios confirming our theory that funds which have a low trail rate are not generally sold by distributors. With a relation in the rules for Registered Investment Advisors (RIA), their numbers will increase leading to an increase in these numbers. We have generally been getting our clients to invest in Arbitrage Funds to take advantage of the lower tax rate of 20% (from 15% earlier). We recommend an STP from Arbitrage funds into equity funds. This may help clients reduce their average cost of purchase in a volatile market. Ideally, we would have waited to start investing in equity. However, with such inflows, it does not seem that a large correction may happen soon. In any case, we only invest in equities if the client has a long enough time horizon else we look for safer investments for them.

Surprisingly, other ETFs have 1.22 cr folios and Rs 5.54 lakh crs assets. This is surprising. Does it mean that these ETFs are used for trading purposes rather than for long term investments? More data on the same can help answer this question.

Debt (Fixed Income) schemes

Debt assets increased to Rs 15.95 lakh crs compared to Rs 14.55 lakh crs last year showing an increase of 9.6%. Money market funds have shown a good increase to rising to Rs 2.25

lakh crs from Rs 1.48 lakh crs. With interest rates supposedly at their peak, gilt funds have hardly shown any movement and have assets under management of Rs 37,000 odd crs.

The last month saw net outflows of 1.07 lakh crs and this month the money came rushing back in to the tune of Rs 1.19 lakh crs. Fifty eight percent of the net inflows was in liquid funds. But a lot of funds came into money market funds. This will likely be stable this month and again the story of outflows will be repeated in end September.