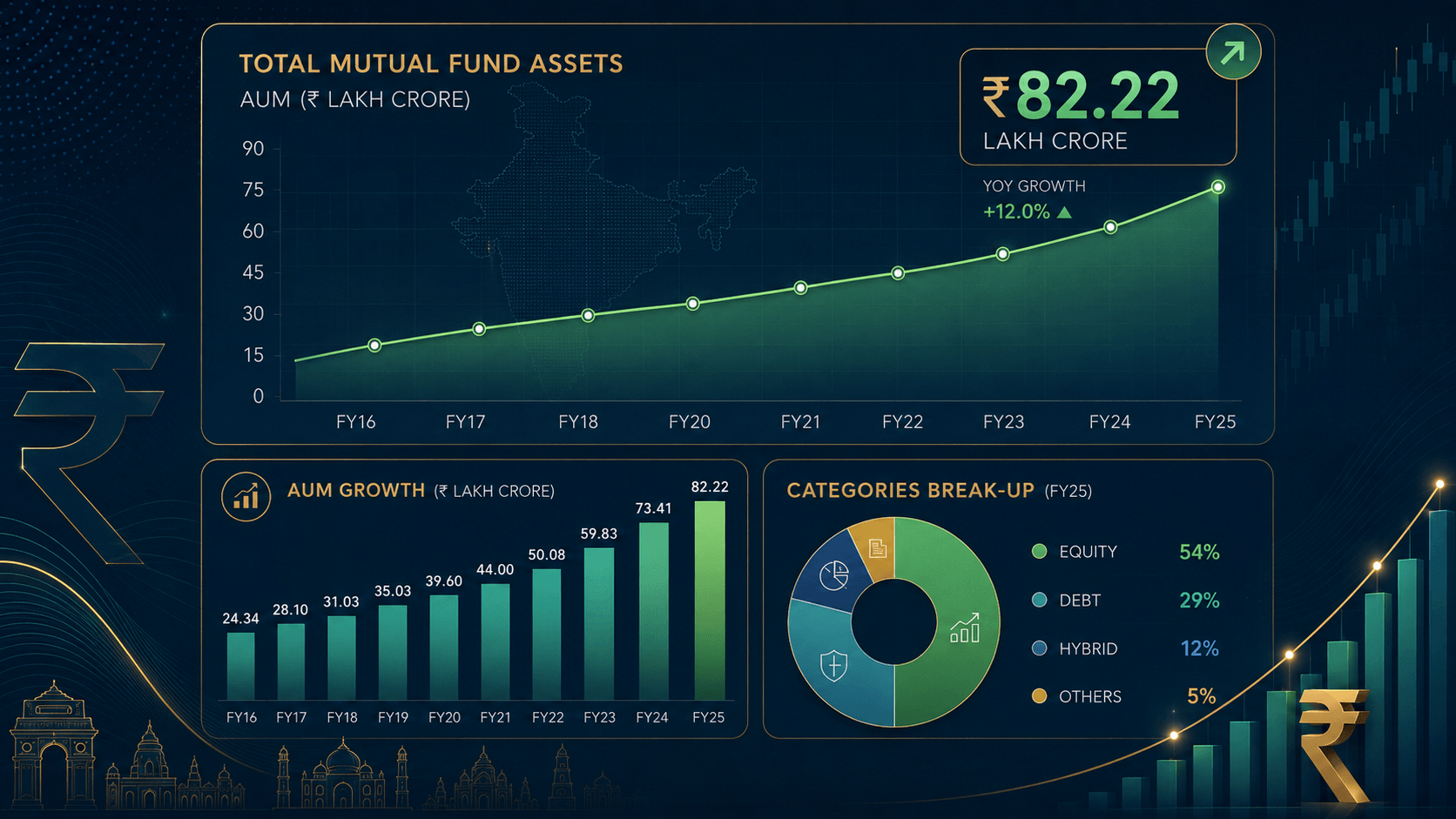

Debt mutual fund schemes continue to elude retail investors. Total inflows into debt mutual funds continue to be higher than equity inflows. Total inflows into debt mutual fund schemes in April 2022 was Rs 743,606 crores vis a vis Rs 73,437 crores in equity schemes including index and other ETFs. Of the 13 crore folios in open ended schemes, almost 94% are in equity schemes and only about 73 lakh folios are in debt schemes. The assets of Debt mutual fund schemes is Rs 13,91,308 crores which is 36% of the total assets in open ended schemes. Clearly, 36% of the assets of all open ended schemes are contributed by only 6% of the folios. No prizes for guessing that debt schemes are generally being bought by either institutional investors or by Ultra High Net worth Individuals or High Networth Individuals. Retail investors seem to be oblivious of these scheme categories which are a great way of getting exposure to diversified and liquid debt portfolios. The average value of a folio in debt schemes is Rs 19 lakhs whereas the same in equity schemes is Rs 1.6 lakhs and hybrid schemes is Rs 4 lakhs. Clearly, the retail investor is giving the entire debt category a miss.

The reasons for the same are not hard to fathom. The commissions earned by distributors on debt schemes will range from 0.1% for liquid schemes to 0.4/0.6% for long term debt schemes. Further, the returns are also volatile as NAV changes with changes in interest rates. Accordingly, it is easier to invest these funds in either fixed deposits with banks and NBFCs or in bonds and debentures. The prices of Fixed Deposits are not marked to market and hence there is no capital gains or losses. The bonds and debentures are marked to market. However, since investors may not look at their demat statements every day, these are unlikely to cause a flutter. The issue with Fixed Deposits is that they are not liquid and premature withdrawals are penalised by NBFCs. Firstly, the interest rate is reduced to the rate that was applicable to the period at the time of making the investment and a further penalty of around 2% is charged for withdrawal. This penalty is not leviable for mutual funds. There is an exit load which may be levied upto one year but there will be no load thereafter. Investors need to consider debt mutual funds schemes for the following benefits:

- Liquidity – Mutual funds provide instant money. Redemption applications made before 3 pm on an working day will provide funds before 10 am of the next working day;

- Lower tax rates – Taxes on long term capital gains (ie capital gains earned after holding the units for more than three years) is 20% after indexation. Accordingly, the tax rate will be much lower compared to an FD for customers whose annual taxable income is more than Rs 10 lakhs

- Diversification – Mutual fund schemes invest in debt papers of different companies in different industries. This assists in diversification of investments. As has been seen with investors of certain banks that faced RBI action, putting all your eggs in one basket is risky and it makes sense to invest in diversified debt schemes rather than chase high returns by investing everything in one issuer and ignoring risk;

- Review of investments: It is the fund manager’s role to keep track of the credit risk of their investments. They are likely to determine an imminent credit event far earlier than a common investor. Of course, given the inherent nature of our market it is possible that mutual fund schemes also end up with credit losses. However, it is likely that the entire portfolio may not get impacted due to such events.

Investors would do well to ensure that their emergency funds are all invested in liquid and ultra short term bond schemes. These are typically 6-8 months of their normal monthly expenses. Further, almost 50-60% of the total debt allocation should be invested in debt mutual fund schemes. Almost all the exposure that is meant for more than three years should be in debt mutual funds. Corporate bond schemes are an ideal investment vehicle for this purpose. Banking and PSU debt schemes will also be ideal for credit risk averse investors. These schemes take exposure to bank debt or those of PSUs, which are considered by investors as safer than private corporates. The average returns of these schemes over three years is 7.29 and that over five years is 7.11. These schemes manage assets of Rs 92,000 crores in April 2022, a miniscule amount compared to the amounts invested in Fixed Deposits which may be more than Rs 14,00,000 crores.

In March 2022, index funds in debt raised close to Rs 3,000 crs. In April, there were no issues of such funds. Clearly, HNIs are using these funds to improve their after tax returns by making use of indexation benefits and staying away from volatile equity markets. It remains to be seen that over a three year period, after markets have corrected by 15% from their peak, whether this will be considered as a smart move. Again, this data clearly shows that the retail investor is missing out on the debt schemes space altogether.

Equity fund flows:

Gross inflows into equity funds fell from 46,400 crs to 32,600 crs. Contrary to popular belief, there is no fall in inflows. There was a large SBI multi cap NFO in March which garnered Rs 8,170 crs. If you take away this NFO, the inflows in March and April are quite similar. In April, ICICI had a thematic fund NFO which raised Rs 3,130 crs. This NFO bolstered the thematic fund inflows in April 2022. The AUM of thematic funds is amongst the highest amongst all categories of equity funds. Thankfully, balanced advantage funds is the only category that is larger than thematic funds. The size of thematic funds and the continued inflows into NFOs suggests that the distribution market in India is still to mature. Investors may do well to review their investments and stay away from NFOs unless the same are new in the market altogether and stick to medium sized schemes with a decent past record of performance. Further, thematic funds by their nature are likely to be more volatile than broadly diversified schemes. While thematic funds can be a part of large portfolios, their presence in portfolios of smaller investors should be a cause of worry. Distributors would do well to stick to diversified funds for their smaller clients.