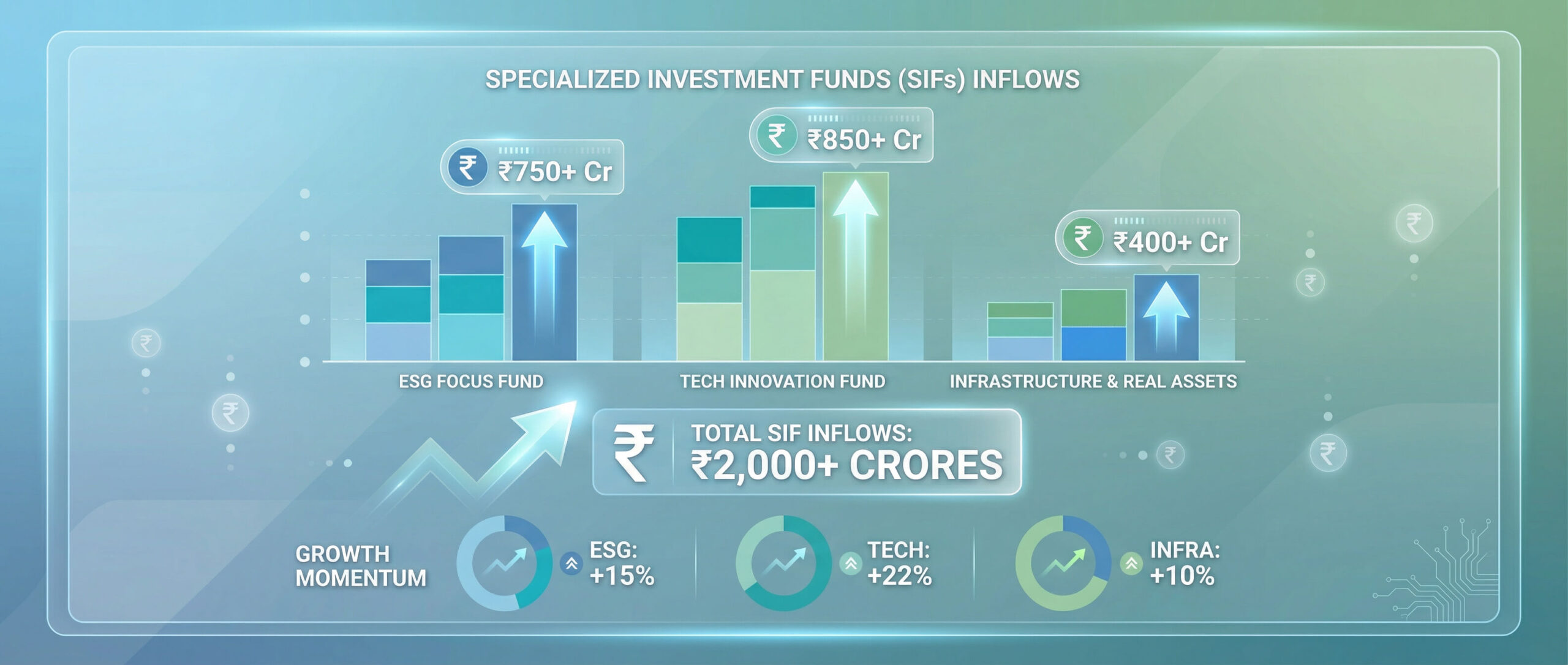

Inflows in Gold ETFs see a massive jump from 11,646 crs to 24,039 crs.

Inflows in debt and Multi Asset Allocation Funds also lead to increase in assets.

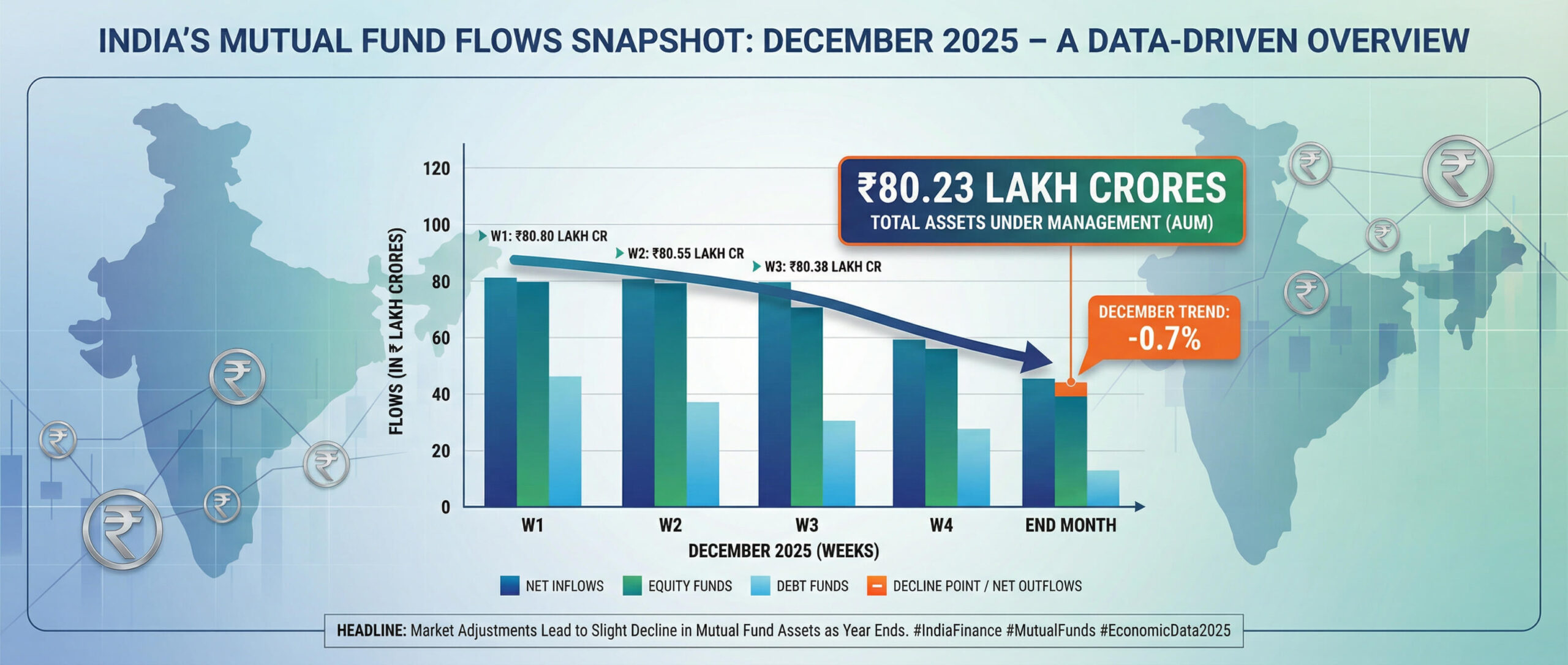

Indian mutual fund industry ended January 2026 with assets of Rs 81.01 lakh crs compared to Rs 80.23 lakh crs in December 2025. The Industry witnessed net inflows of Rs 1.56 (-0.66) lakh crs, with debt schemes showing inflows of Rs 0.74 (-1.32) lakh crs and equity and hybrid schemes showing net positive inflows of Rs 24,028 (28,054) crs and Rs 17,356 (10,756) crs respectively. Equity schemes saw a decrease in assets to Rs 34.87 (35.72) lakh crs. This was mainly due to negative performance of the equity markets. Nifty 500 moved down by 3.27% (+0.26%) and Nifty 50 also decreased by 3.04% (-0.28%) with mid caps down by 3.5% (-0.53%) and small caps down by 5.5% (-0.28%). One year returns for all indices are slightly positive except for small caps. Three and five year numbers continue to show healthy returns.

Mutual Fund Industry Overview

🔹 Monthly flow and AUM trends:

Equity Mutual Funds :

– Net flows in equity schemes decreased to Rs 24,028 crs from Rs 28,054 crs last month. Though there have been no negative inflows for almost five years. Flows in NFOs were subdued at Rs 806 (3,568) crs.

– Net inflows in various categories were as under and have mostly declined compared to last month. ELSS funds saw net outflows:

– Sectoral/Thematic Funds: Rs 1,042 (946) crs

– Flexi-Cap Funds: Rs 7,672 (10,019) crs

– Small-Cap Funds: Rs 2,942 (3,824) crs

– Mid-Cap Funds: Rs 3,185 (4,176) crs

The net inflows have dipped below the SIP inflows of Rs 30,000 crs showing that investors are booking profits and moving out of equity funds.

📌 #EquityFunds #MutualFunds #WealthCreation #LongTermInvestment #EquityMarket #ELSSschemes #Equityschemes

Debt Funds: Inflows due to the beginning of the financial year/quarter

📉 Key Trends in Debt Funds:

– Total debt fund AUM was Rs 18.09 (18.10) lakh crore, almost similar to last month. The average assets in the month were higher suggesting a sell-off in the last few days of the month.

This category saw a net inflow of Rs 0.74 lakh crs compared to an outflow of 1.32 lakh crs last month. Liquid, Money market and overnight saw inflows while corporate bond funds saw outflows.

#DebtFunds #InterestRates #BondMarket #FixedIncome #FinancialPlanning

Hybrid & Passive Funds:

– Hybrid funds’ assets were almost the same at Rs 11.0 lakh crs. Net inflows into hybrid funds stood at Rs 17,356 (10,756) crs, led by Multi Asset Allocation funds, which saw inflows of Rs 10,485 (7,426) crs. Inflows in these funds have doubled in two months. Arbitrage funds inflows also were at Rs 3,293 crs (126). Again investors are chasing returns with MAAF and Gold ETFs seeing huge inflows.

📌 #HybridFunds #Diversification #RiskManagement #BalancedInvestment

Passive mutual funds:

Inflows into Gold ETFs have soared to 24,040 crs compared to 11,646 crs in December 2025. Inflows in index funds were Rs 27.3 crs and those in other ETFs were Rs 15,005 crs (13,199).

Fund of Funds Schemes (FoFs):

FoFs collected almost Rs 11,250 (10,250) crs of net inflows. ng at sectoral or thematic funds would be wise to choose from amongst these funds.

🧐 Way forward

Gold ETFs and Multi Asset Funds have seen an even higher increase in inflows in one month due to the good performance of gold over the last 12 months. Investors are falling prey to the FOMO phenomenon. Chasing returns is not the way to earn above average returns or beat the benchmark. Asset allocation and re-balancing is the way to go. Say you have invested 60:25:15 in equities, debt and gold. Now gold has run up by 100% whereas debt is up 7% and equities are flat. The portfolio will show a return of 16%. The portfolio value will be Rs 116 with an asset allocation of 51:23:26. If we re-balance the portfolio, we will sell gold and invest the same in equity and debt and bring the asset allocation back to the original ratio. This ensures that you sell the asset class which has increased in value and buy the other asset class which is lower in your portfolio. Asset allocation ensure that you are present in all asset classes and reap the benefits of any sudden and great upturn in values and re-balancing periodically ensures that you sell high and buy low. This simple discipline may go a long way in getting above average returns.

About EquiZen

EquiZen, a registered mutual fund and PMS distributor, offering personalised financial solutions with a focus on safety and transparency. We aim to assist you to achieve financial freedom, the freedom to do what you want and achieve your dreams. We do not push financial products but believe in utilising them judiciously to meet your needs. Learn more at www.equizen.in or contact us via +91 9820605203 or sanjay@equizen.in.